Two years ago, my co-founder Jonathan and I headed into the Colorado mountains looking for adventure, but what we walked out with was a business idea. Maybe it was the death-defying rafting trip or that rustling in the woods, but our conversation turned to family and how important it was to protect them. We both have young kids and we started talking about how painful the process for getting life insurance was.

We decided to dig in. For months we met nights and weekends, learning everything we could about the industry. We spoke with large insurance companies, lawyers, agents, reinsurers, investors, friends, long lost cousins…anyone who could help us better understand the space. As an aside, most of the time when you research a business idea you end up concluding it’s not the opportunity you hoped for. This was the exact opposite.

What we found was shocking — an industry largely still void of technology, that hasn’t meaningfully changed in decades. Surely an industry as large as life insurance with $130B+ in annual revenue and trillions of dollars in assets in the U.S. alone had been transformed by the digital revolution. But it had not been.

One of my heroes, Teddy Roosevelt, admired “the one who is actually in the arena; who strives valiantly, who spends himself in a worthy cause…while daring greatly.” We decided to go all in.

The Oldest of Old School

12 of the top 15 life insurance carriers today were founded in the early 1800s. To put that in context, we’re talking industrial revolution times. Before the invention of the steam engine, locomotive, the telephone, and combustible engine. That is some serious staying power. By contrast, only 12 of the top 100 companies from the early 1900s remain today.

>

There is simply no other industry with these same statistics. On the one hand, it’s amazing that these companies still exist and provide value to so many consumers. Kudos to them. On the other hand, so much has changed over the last 200 years like major causes of death, coverage preferences, consumer preferences, and technological advances, just to mention a few. We think it’s time for a new kind of insurance company, built from the ground up with the best of modern technology for a digital consumer.

Wait, What?

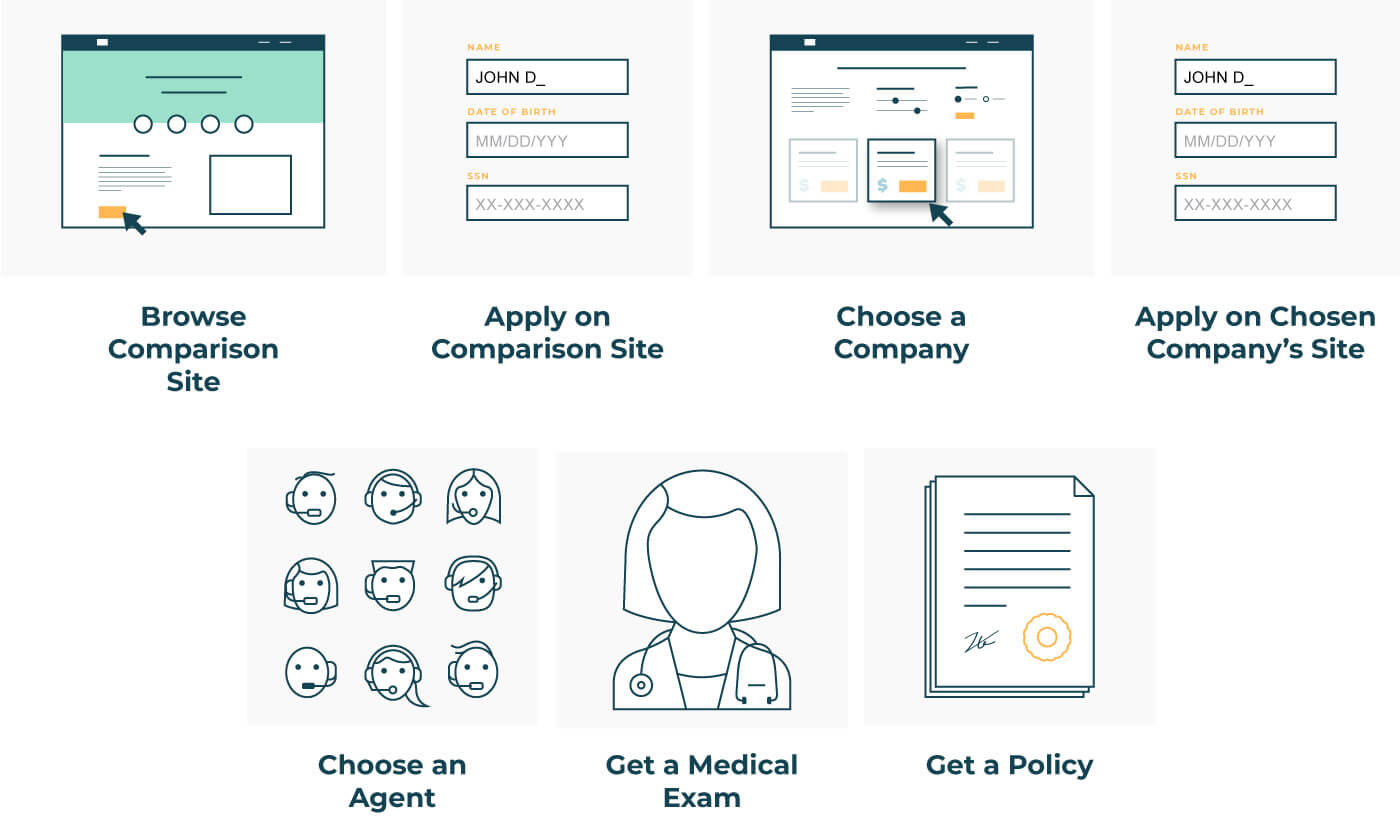

Many people we initially spoke with thought they could already get life insurance immediately online. We put them to the test and asked them to actually try to purchase.

You see, most companies have the applicant provide a small amount of information upfront, making the customer feel as if they can complete an online application. But, that’s just the beginning. Imagine you could only get airfare estimates online, but actually had to move offline and meet with a travel agent to make reservations and book tickets.

The applicant gets an estimated quote and is then told they need to schedule a call or in-person meeting with an agent. Wait, what? After a medical exam and typically 3–4 weeks of back and forth with agents, underwriters, and a medical exam, you too could possibly, maybe, be the proud owner of a life insurance policy.

Enter Bestow

We set out to build a new solution from the ground up, and that’s exactly what we’ve done. Approximately 5,000 Diet Cokes, 80 boarding passes, countless mini-basketball tournaments, and too many dad jokes later, we’re ready to share what we’ve been working on.

Our purpose is to create a world where every life is valued and protected. What does that mean exactly? We aim to help people protect their people by making that choice easy and intuitive. And to make it accessible to millions of families who would otherwise go uninsured.

We’ve built Bestow knowing that in order to reshape our industry we must deliver meaningful product differentiation and change the underlying cost structure of a life insurance company. And we are well on our way.

Starting with product, we developed (with our insurance partners) one of the first all-digital term life product. We didn’t take a product that was already sold offline and just put it online. We took a first-principles approach starting by refining the application process and creating a delightful user-friendly experience.

At the same time, we tackled head-on possibly the most difficult problem for the industry; how do you take something that has been manually processed for centuries by skilled underwriting experts reviewing detailed information and medical records, and automate and improve it? Unlike P&C or health insurance products that tend to sell in one-year increments, we are underwriting risk at a single point in time for decades of coverage. It’s important we get it right.

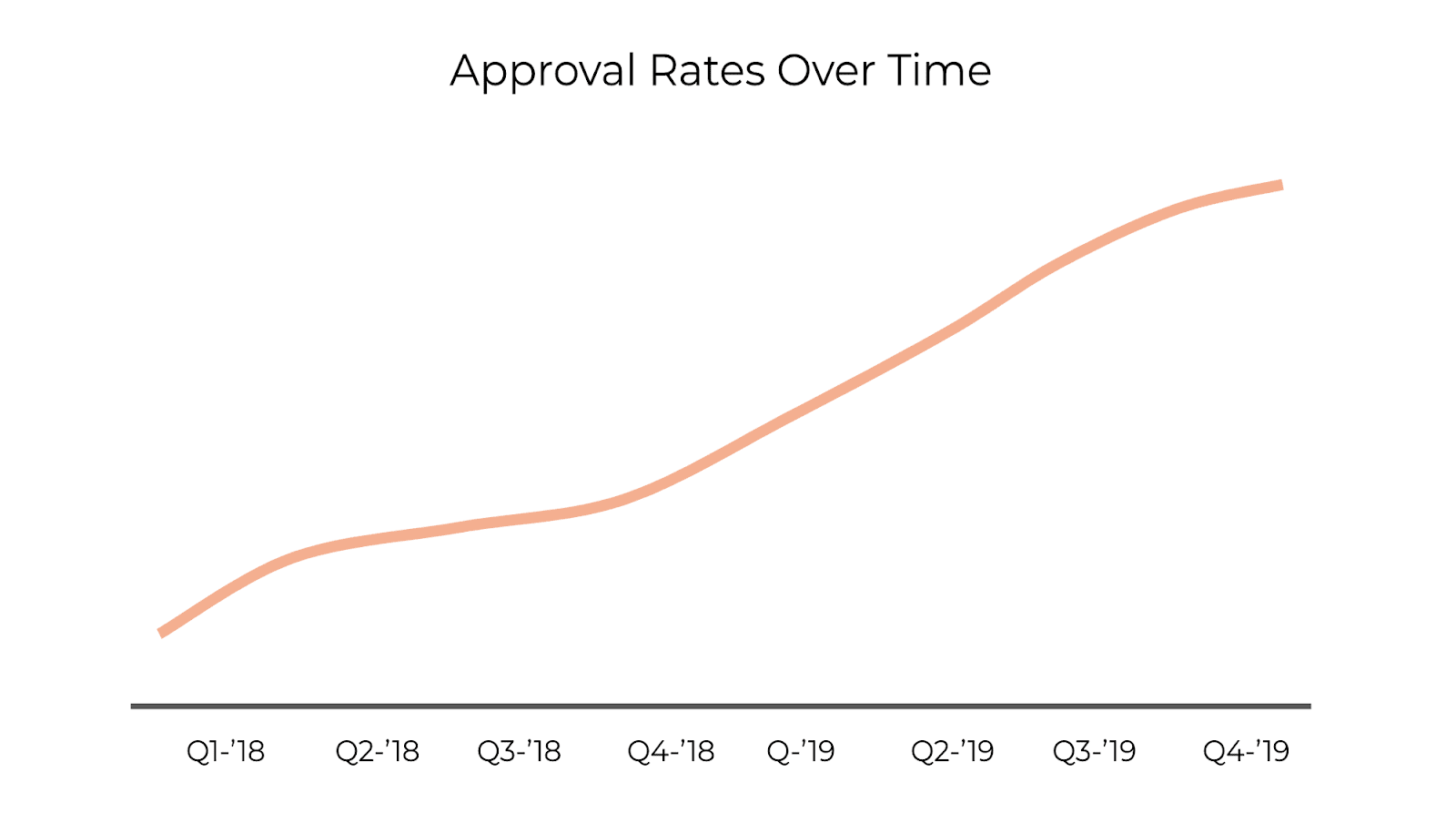

Starting with first principles and in collaboration with best-in-class insurance partners, we sourced data and developed algorithms to automate the process. We didn’t want to build a solution that worked for only 10 or 20% of applicants, forcing the majority to get a medical exam. We wanted everyone to avoid the doctor’s visits, blood draws, and agent meetings.

While we originally started at a lower eligibility rate, we quickly improved our algorithms and ability to instantly underwrite more types of risk.

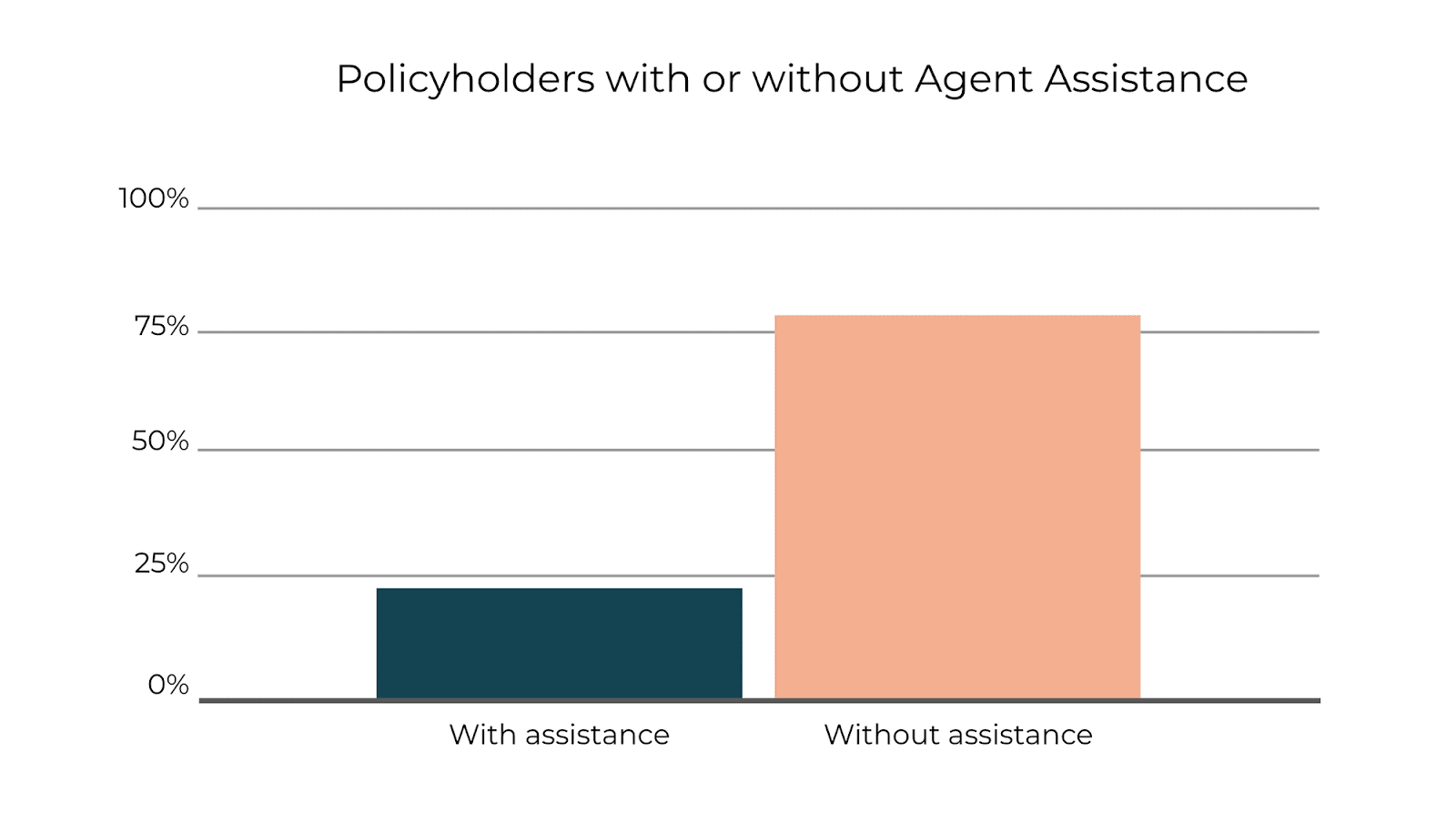

We’re also disproving the often-repeated industry adage “life insurance isn’t bought, it’s sold.” While our view is that agents and advisors have, and will remain, essential in helping people get proper life insurance coverage, our data demonstrates that there is a large customer base who knows what they want and prefer to buy directly, without speaking with one of our licensed (and non-commissioned) agents.

And, by the way, when you do let consumers self serve you get NPS scores and reviews like this:

*NPS score as of 12/11/2021

Bestow is breaking out. We have built a digital life insurance company from the ground up, developing products and a platform that will prove to make a seismic change for the industry, and more importantly for the consumer. We’ve expanded to 49 states and are continually developing products and services that will change the way Americans think about life insurance.

Curious about the Bestow experience? Start with a free instant quote and see just how easy applying for term life insurance can be.